On top of Kentucky’s state flat income tax rate of 4.0 in 2024, some of its counties and cities also impose an additional local tax. Kentucky refers to these as Occupational License Fees/Taxes, and these apply to all employees, including household employees.

Each city has its own requirements and method to pay. For example, Louisville Metro has combined taxes totaling 2.2% for employees who work and live there or a 1.45% tax rate for non-resident employees. This amount is withheld from an employee’s paycheck, and then remitted to the city quarterly by employer by the following dates.

Paying nanny taxes in California includes payment to the IRS for federal taxes as well as payments to California’s Employee Development Department (EDD).

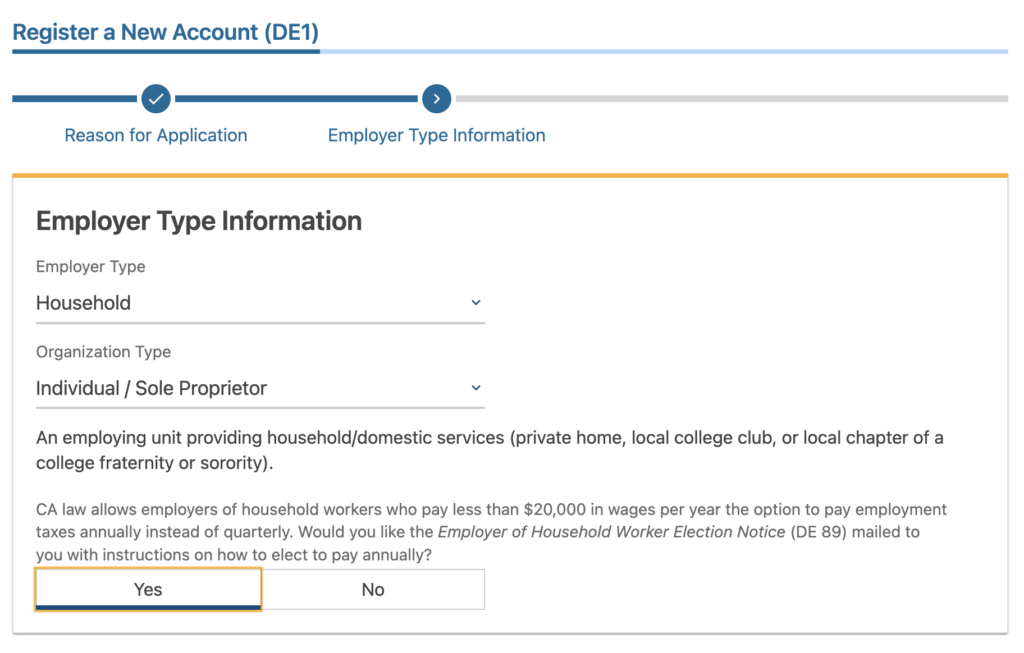

Create an account with California EDD, which will be used for California specific filings. Use the “Enroll” button under e-Services for Business to create a user name and password.

Once you have paid $750 or more in a quarter, you must register with the state of California for an Employer Payroll Tax Account Number. To do log in using your e-Services username and password created in the previous step.

For “Reason for Application”, select “New Hire”. The following page will prompt you for “Employment Type”, where you can select “Household”.

If you plan to pay $20,000 or less a year to all employees, you can elect to pay once a year, rather than quarterly. In this case you will be considered an “Annual Payer” rather than a “Quarterly Payer”

4. If you and your nanny agree to withhold income tax, have your nanny fill out forms W-4 and DE 4 for withholding elections.

6. Form I-9 is used to verify that your nanny is legally able to work in the US. You do not need to submit this form but must retain it in your records.

Each pay period

Each pay period the person you need to pay is your nanny. Pay her the Net pay amount via cash, check, or direct payment initiated from your bank.

Report wages and taxes for Jan – March by April 30. If you are a quarterly payer, you will also pay at this time.

July

Report wages and taxes for April – Jun by July 31. If you are a quarterly payer, you will also pay at this time.

October

Report wages and taxes for July – Sept by Oct 31. If you are a quarterly payer, you will also pay at this time.

January

Report wages and taxes and pay for Oct – Dec by Jan 31. Both quarterly and annual payers will pay at this time.

The CA taxes are SDI (State Disability Insurance), ETT (Employment Training Tax), UI (Unemployment Insurance, shown as SUTA on pay statement), and PIT (Personal income tax, shown as CA Income Tax).

For quarters that you do not have wages, you must still file the report. You can close your account if you no longer plan to have any employees.

Paying Federal Taxes

The federal taxes are Social Security, Medicare, Federal Unemployment (FUTA), plus any income tax withheld from your nanny’s pay.

The balance of those federal taxes is paid with your personal income tax return due April 15, by adding Form Schedule H.

However, if the amount of taxes to be owed over the course of the year is greater than $1,000, you should pre-pay the IRS along the way to avoid a tax underpayment penalty. There are a couple of ways to do this:

Option 1 – Update your withholding: If you are a W-2 employee, you can update your own W-4 election with your employer to have the additional tax amount withheld from your pay.

For the example pay statement in the previous section, the household employer can request an additional $63 (employee + employer portion of SS and medicare + federal income tax withheld) withheld each week from their pay. This amount gets paid to the IRS on their behalf by their employer.

Option 2 – Pay Estimated Taxes quarterly: You can alternatively make Quarterly Estimated Payments to the IRS yourself by April 15, June 17, September 16, and January 15. The DirectPay option allows you to quickly pay without creating an account, while creating an account will allow you to track previous payments. EFTPS is another option geared toward businesses but also can be used by individuals who wish to schedule all payments for the year.

Note that the amounts pre-paid are a best estimate. Form Schedule H will determine the exact amount owed and reconcile any differences.

Annual – Creating a W-2 for your nanny

As a household employer, you will need to provide your nanny with a W-2 by January 31 for the prior tax year.

A W-2 can be created and filed using the online tools from the Social Security Administration, which will contain both the federal and state information she will need in her own tax return.

California requires employers to carry Workers’ Compensation insurance. This is separate than CA and federal taxes, and not reflected on the pay statement.

Follow the payment schedule required from your insurance provider for this.

Some states have State Disability Insurance (SDI) or Family Leave contribution requirements. These additional taxes fund programs which can provide monetary benefits to your nanny if they have a qualifying life event.

California

CA requires employee contribution of SDI. Alternatively, it is allowed for employers to pay this for their employees.

Colorado requires contribution to Family and Medical Leave Insurance Program (FAMLI) at a rate of .45% for small employers. Alternatively, it is allowed for employers to pay this on their employee’s behalf.

Connecticut requires contribution to CT Paid Leave at a rate of .5% for small employers. Alternatively, it is allowed for employers to pay this on their employee’s behalf.

MA requires contribution of Paid Family & Medical Leave, withheld from your nanny’s paycheck. Alternatively, it is allowed for employers to pay this on their employee’s behalf.

Provide the document generated by the online tool to your nanny, babysitter, or other household employee. Your household employee will use this for their own tax returns.

Steps to Generate a W-2 for your nanny

Gather Form I-9 your nanny completed around first day of employment. You will need this for your employee’s SSN and home address.

Download the completed Form W-2, and provide this to your nanny for her own tax return.

What to enter in each W-2 box

Boxes a – f Employee and Employer identification info

Enter name, addresses, and other information to identify you and your nanny in Boxes a, b, c, e, and f. Leave Box d blank.

You can find your employee’s SSN and home address on Form I-9 that your nanny completed around first day of employment.

Box 1

The amount you need to enter into Box 1 is listed as Taxable wages on the Paycheck Nanny app.

This includes regular, overtime, bonus or other taxable pay for your nanny. If you are paying all of the FICA taxes on your nanny’s behalf, instead of withholding half of total Social Security and Medicare from their paycheck, the employee portion of FICA is also included in this amount.

This does not include SIMPLE IRA retirement plan contributions, Health Insurance benefits, or Commuter benefits for parking or mass transit costs.

Box 2

Enter in the amount of federal income tax withheld. If you did not withhold income tax from your employee’s paycheck, this will be 0.

Box 3

Social Security wages is often the the same as the Taxable Wages specified in Box 1.

One exception is if you as the employer also pay the employee’s portion of FICA for them. In this case, Box 1 value will be greater than Box 3. In this situation, include the extra employee portion of FICA paid by you in Box 1 but not Boxes 3 or 5.

Another exception is if participating in a SIMPLE IRA retirement plan, then your nanny’s contributions are included as Social Security and Medicare wages, but not taxable wages in box 1.

Box 4

Enter the amount of Social Security tax withheld from your employee’s paycheck.

Don’t worry about the employer portion when creating a W-2. That will come into play when you file form Schedule H with your own tax return.

Box 5

The Medicare wages will be the same as Box 3, as long as your nanny has earned less than $176,100 in 2025 from you, which is the cap on Social Security wage base but not Medicare.

Box 6

Enter the amount of Medicare tax withheld from your employee’s paycheck.

Don’t worry about the employer portion for creating a W-2. That will come into play when you file form Schedule H with your own tax return.

Box 12

If you employee has contributed to a SIMPLE IRA, specify the employee’s total contribution with code S. Note that any employer contribution to the SIMPLE IRA is not included on Form W-2.

If you have reimbursed Health Insurance costs for your nanny, enter the available amount in Box 12 with code FF, which is reserved for QSEHRA (Qualified Small Employer Health Reimbursement Arrangement) benefits. Note that the amount available should be entered here, even if the employee did not request reimbursement of the entire amount.

Box 13 Retirement Plan

Check the Retirement Plan box if your nanny has SIMPLE IRA or other retirement plan contributions.

Box 14 Other

Use Box 14 to provide record of additional employee paid taxes, such as Disability or Family Leave taxes for states that have those.

Employees who itemize deductions on their tax returns may be able to deduct these amounts from their income tax liability. If an employee chooses to take the standard deduction when filing their own personal income taxes, then they can ignore these values.

Notice that employer contributions to Family leave or disability plans, such as DC Paid Family Leave, are not included in Box 14.

California: Enter in the amount withheld from your employee’s paycheck to CA State Disability Insurance Tax as “CA SDI”.

Colorado: Report employee CO FAMLI premium deductions as “FAMLI”.

Connecticut: Specify CT Paid Leave employee contribution amount as “CTPL”.

Delaware: Indicate any employee contributions to Delaware Paid Leave (PFML).

Massachusetts: Indicate the employee paid portion of Family Medical Leave contributions with Description of “MAPFML”.

New Jersey: Follow NJ W-2 guidance to include worker contributions for UI, SDI, and Family Leave.

New York: Include employee contribution of SDI as “NY SDI”. Also indicate the Employee contribution of “NY Paid Family Leave”.

Oregon: Specify the amount of Paid Leave Oregon employee contribution.

Pennsylvania: Indicate Pennsylvania State Unemployment Insurance employee withholding as “PASUI”. Alternatively, “PA UC” can be used to abbreviate PA Unemployment Compensation. These indicate the same program.

Rhode Island: Include employee contribution of SDI as “RI SDI”.

Washington: While WA also has a Paid Family & Medical Leave program, it does not have a state income tax (for the employee to potentially deduct this amount from). So employee paid portions of this can be added as an FYI, but the WA Paid Family & Medical W2 Leave guidance does not specify it as required.

Box 15 Employer’s

Enter the abbreviation for the state of employment. For the ID, enter in your state issued Employer ID if your state has issued you one. Otherwise, re-enter your federal EIN.

Box 16 State wages, tips, etc.

If your state has a state income tax, enter in the taxable wages the state will consider. In most cases, this is the same amount as in Box 1.

Leave this blank if your state does not have an income tax.

Box 17

Enter in the amount of state income tax withheld. Leave this blank if you did not withhold any state income tax from your employee’s paycheck.

Box 18 Local wages, tips, etc.

If your locality has local income tax, in addition to the state income tax, enter in the taxable wages the state will consider. In most cases, this is the same amount as in Box 1.

Leave this blank if your city is not subject to additional local income tax.

Box 19 Local income tax

Enter in the amount of any local income tax withheld. Leave this blank if you did not withhold any state income tax from your employee’s paycheck.

Box 20 Locality name

Enter in the locality name for local income tax, if applicable.

W-2 FAQs

What else do I need to do for tax time?

With your own tax return, you will need to include form Schedule H and remit taxes withheld and owed at that time.

For a full checklist of how to pay your nanny legally, see here. View this information and more in the Paycheck Nanny app for iOS.

If you are employing a nanny or caregiver, each pay period you may be withholding taxes, such as Social Security, Medicare, or income tax from your employee’s paycheck.

So what do I do with the withheld taxes?

As a household employer, you must pay these taxes to the IRS in one or more of the following ways:

(If needed) Have a similar amount withheld from your own paycheck, which your employer will pay to the IRS.

(If needed) Pre-pay estimated amount via quarterly Estimated Taxes.

(Always needed) Reconcile final amount in your own yearly Tax return.

Option 3 above is necessary in all cases of household employment where taxes are owed. The final amount is calculated via Form Schedule H which should be included in your usual yearly tax return.

Note some states additionally have state specific taxes that need to be paid directly to the state, typically each quarter.

In what cases do I need to also pay taxes ahead of my yearly tax return?

Options 1 or 2 are necessary in cases where the amount of taxes withheld would cause your tax owed to the IRS with your yearly Tax return to be $1,000 or more that you have not yet paid.

As an example, if your summer time nanny will gross $6,000 from you, the amount of Social Security plus Medicare tax withheld would be $459, and your share of employer taxes would be similar. Say she has $0 federal income tax withheld because her income is not high enough. In this case, you could solely pay the taxes in a lump sum with your yearly tax return.

Now, if you also hire another nanny during the school year who makes $5,000 for care after school and during school vacations. The combined taxes withheld for the year will be greater than $1,000. In this case, the IRS will want that money paid prior to your yearly tax return.

Option 1: Extra withholding

If you’ve determined that more than $1,000 would be owed, there are two options to pay this during the year.

If you (or your spouse if filing jointly) are a W-2 employee, you likely are already getting taxes withheld from your paycheck by your employer. In this case, an easy option is to request your employer withhold an extra amount each paycheck to account for this money, and they will then pay this amount to the IRS on your behalf. Do this by requesting to update Form W-4, Employee’s Withholding Certificate, with your employer at any time of year.

If your nanny’s pay fluctuates each week and you do not know the exact amount of tax that will be paid, that is ok. You will still finalize any additional amount owed or overpaid during the year when you file your yearly tax return.

Option 2: Estimated Taxes paid quarterly

The alternative option if you will owe more than $1,000 in taxes is to pay Estimated Taxes quarterly. This is paid directly to the IRS, due on the following dates.

April 15, 2024

June 17, 2024

Sept. 16, 2024

Jan. 15, 2025

Estimated Tax Payment can be made online via any of the options at https://www.irs.gov/payments. The DirectPay option allows you to quickly pay without creating an account, while creating an account will allow you to track previous payments. EFTPS is another option geared toward businesses but also can be used by individuals who wish to schedule all payments for the year.

The full IRS guide to Estimated taxes can be found at:

If you plan to pay your nanny $2,400 or more in 2022, in most cases you are considered to be a household employer. While this comes with extra benefits to you and your nanny, it comes with some extra paperwork.

A full service payroll provider can file these forms on your behalf for a price.

But if you are not interested in paying the extra price of a nanny payroll provider, you can do it yourself. All of these forms are free and easy to file.

1. I-9 Form

Time to complete: 15 mins. Cost: Free

Form I-9 is used to verify that your nanny is legally able to work in the US. First, print out an I-9 form for your nanny to fill out after accepting the job offer but no later than the first day of work.

This form indicates documentation you as an employer need to inspect (Drivers license, SS Card, etc). You do not need to submit this form but must retain it in your records.

The list of New Hires is used by agencies operating child support, unemployment programs, and workers’ compensation services.

4. Nanny Contract

Time to complete: 1 hour. Cost: Free, or purchase a template

A written Employment Contract, also known as a Nanny Contract, can clarify expectations and avoid conflicts. It should include things such as hourly and overtime pay rates, pay frequency, taxes withheld, daily duties and other expectations, PTO, and required leave notice.

5. Other State Specific Forms

Time to complete: 1 hour. Cost: Free

Depending on your state, you may also be responsible for other state employment taxes, such as State Unemployment Tax.

Next steps

After the forms are filed, there are also weekly tasks to track hours worked and calculate taxes and how much to pay your nanny. The Paycheck Nanny app helps with these tasks and provides guidance in navigating nanny taxes. Find it in the Play Store for Android devices or the App store for your iPhone and iPad.

California, Colorado, District of Columbia, New Jersey, New York, Massachusetts, Oregon, Rhode Island, and Washington also have State Disability Insurance and/or Family Leave contribution requirements. See https://paychecknanny.com/blog/disability-or-family-leave-taxes/ for details.

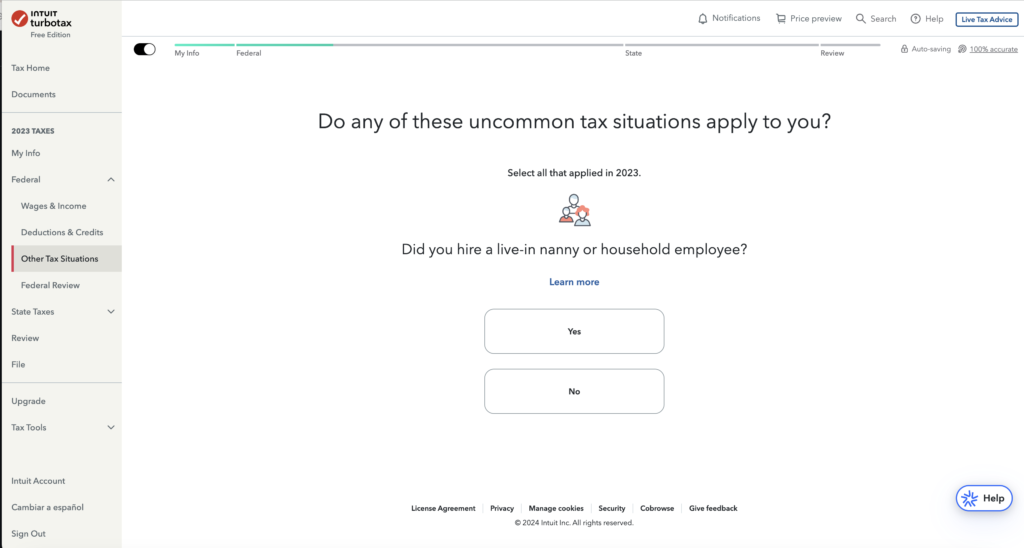

It’s tax time again! If you had a nanny, babysitter, or any household employee last year, you need to file Form 5471 Schedule H with your tax return if you answer yes to any of the following.

In the 2023 tax year, did you:

pay any one household employee cash wages of $2,600?

withhold federal income tax for any household employee?

pay total cash wages of $1,000 or more in any calendar quarter to all household employees?

What this form does is capture how much you have paid to a household employee and the taxes you have already withheld. With that, it will determine the amount you owe to be included as part of your personal tax return.

If you are using the Paycheck Nanny app for iOS, your nanny’s gross earnings for Last Year on found at the top of the Pay History tab when the “Last Year” time range is selected.

If you are filing your taxes with TurboTax, H&R Block or other tax software, it will walk you through entering the information needed.

TurboTax captures this information under “Other Tax Situations” and requires TurboTax Deluxe to complete this form. If using the TurboTax free edition, it will prompt you to upgrade if you indicate that you had a household employee last year.

If you are not using tax software, you can alternatively download the Schedule H itself and also the Instructions for Schedule H from the IRS website.

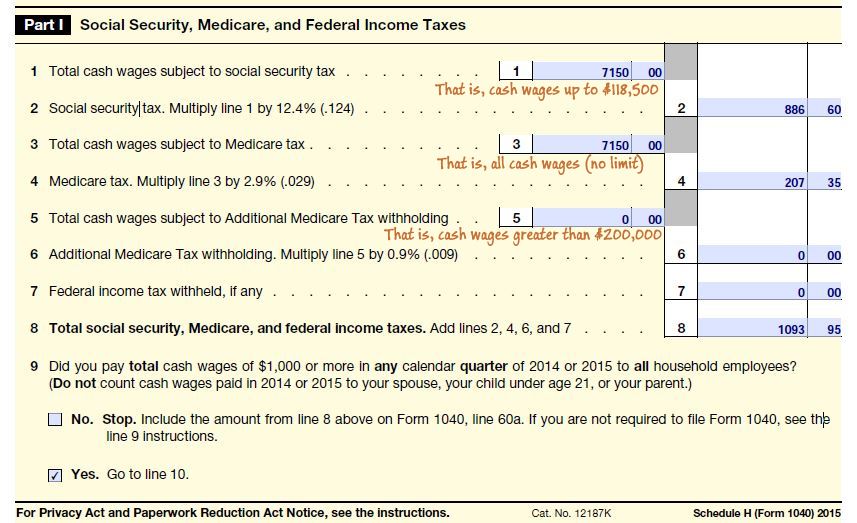

Schedule H – Part I

Below is an example of what Part 1 of Schedule H looks like when filled out, with some hints added in-line. This example is for a nanny who worked during school vacations and made $7,150 gross cash wages. While the forms below walk through an example from a prior year, Form Schedule H with your 2023 tax return will look similar, except that the limit for item 1 (Total cash wages subject to social security tax) has increased.

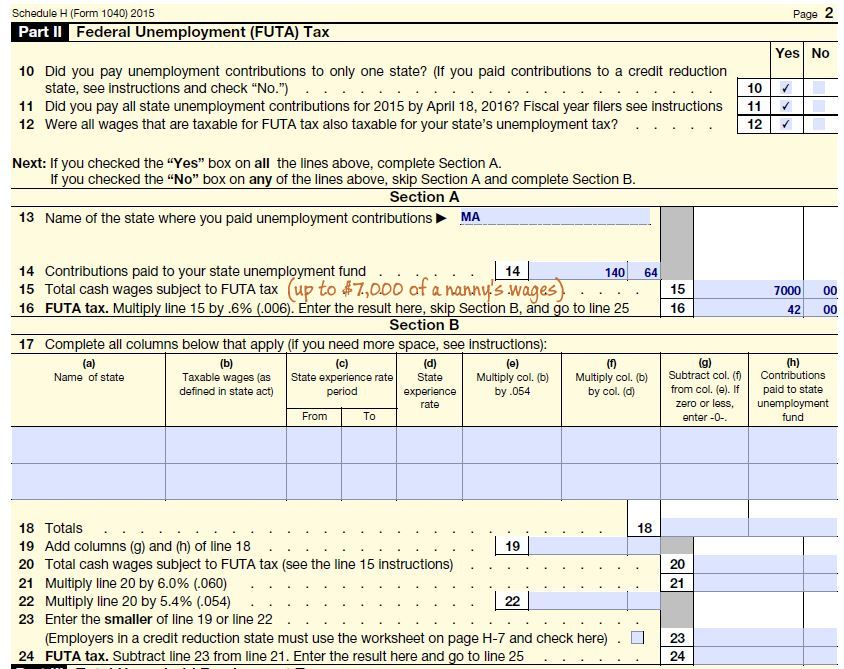

Sch H – Part II

Part II calculates Federal Unemployment (FUTA) tax owed. The calculations will vary depending on your state. For the 2023 tax year, California, New York, and the US Virgin Islands is considered a “Credit Reduction State” for Federal Unemployment (FUTA) Tax purposes. If you have employed a nanny elsewhere, skip to the section for FUTA for all other states.

FUTA for CA, NY, & US Virgin Islands

For California, New York, or US Virgin Islands, in Schedule H – Part II, leave Section A blank and fill out Section B instead.

Note the states which are ‘credit reduction states’ varies from year to year.

FUTA for all other states

For all other states, you will be paying .6% (.006) of your nanny’s first $7,000 wages in FUTA. So this means the maximum amount of FUTA you will need to pay is $42 for the year. Below is an example from Massachusetts, a non-credit reduction state. Notice if you can answer No to questions 10, 11, and 12, then you should leave all of Section B blank.

Schedule H – Part III

Than after you fill in the calculations in Part III, this Schedule H and payment owed goes along with your personal 1040/1041 tax filing as part of your yearly household employer duties.

State Unemployment Tax, also known as SUTA, is an employer paid tax that some states impose. SUTA can be in addition to FUTA (Federal Unemployment Tax) or instead of it.

The rate you pay for SUTA will be based on your state plus your history as an employer. You will be sent your rate information when you register with your state.

Alaska, New Jersey, and Pennsylvania also have a small SUI tax which is employee paid